Many new business owners can get a shock with the minimum insurance requirements we all have, even for a seemingly basic business.

As you enter complex fields with specialised needs, the list of insurances and ensuring quality policies is critical to keep your business running and compliant.

Running a business involves moving parts, constant change, surprises, and risk.

From property damage to cyber threats, legal claims to injured staff, the right insurance can mean the difference between a temporary hiccup and a financial blow that cannot be recovered from.

It is critical to have the right broker, insurer, and proactive risk management plan. These can ensure you get the right cover, avoid overpaying, and protect your business as it grows.

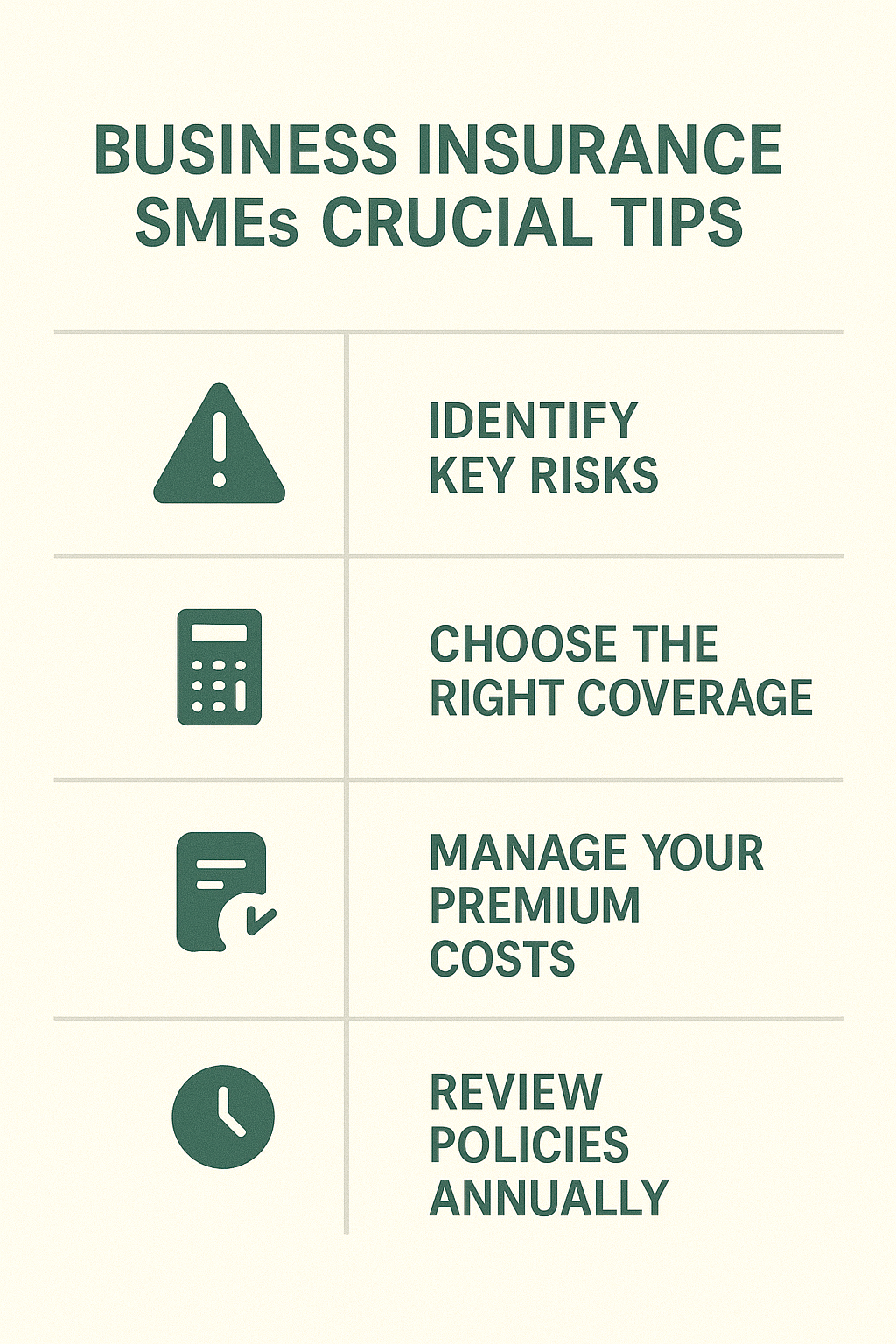

This guide walks you through:

- The essential types of insurance for Australian businesses

- How to choose a quality insurance broker

- Why your premiums go up and how to bring them down

- The critical importance of annual insurance reviews

👉 Need Help and Advice With Your Business Insurance? Get Help Here.

Examples of SME Business Insurance Australia

First, let’s look at some examples of business owners who could have been sued or lost significant money if they had not had the right coverage in place.

- An e-commerce store selling baby products recalled a batch of baby carriers after reports of faulty buckles breaking under pressure. The recall involved refunding customers, shipping replacements, and issuing public safety warnings. The company covered its losses without suffering severe financial strain thanks to recall insurance.

- A local tradesman working on a commercial building site locked up his excavator for the night. When he arrived the following day, his $60,000 machine had been stolen. He first needed to get a new machine urgently, but his contract also would have made him liable for delaying the work. He could claim on his policy and had a new machine within a few days, allowing him to avoid penalties.

- A contractor was engaged to construct a commercial fencing project. A separate worker on the site twisted their knee and back when they stepped backwards into an uncovered hole the contractor had drilled. The matter was settled for over $100,000, including administrative and medical expenses.

- A significant storm caused severe damage to a café. The owner was forced to close his business and repair the damage. The business owner received $30,000 for building contents, $20,000 for loss of income, $3,000 for lost wages, $20,000 for additional repairs, and $500 for the appraisal cost.

Essential Insurance for Australian SMEs

Depending on your industry, the size and structure of your business, your needs will var,y but these are the key insurances most small to medium businesses should consider:

-

Public Liability Insurance (PL)

This insurance covers injury or property damage to third parties caused by your business. It is essential for any business with a physical presence or customer interaction, including one-off functions/events. If someone is injured at a place you are in control of, you are liable!

-

Professional Indemnity Insurance (PI)

PI protects service-based businesses against claims of negligence or breach of duty. Think consultants, designers, brokers, advisers—anyone offering advice or a service can be sued and liable for ‘deemed’ damages.

-

Workers Compensation

A legal requirement if you have employees. It covers wages and medical costs if a worker is injured on the job. Many owners don’t know they can be included in this insurance.

-

Business Interruption Insurance

This is a fantastic cover that protects you from loss of income if your operations are halted due to events like fire, flood, or equipment failures. This is critical, particularly for businesses such as restaurants/cafes that rely on physical presence to generate income, and even manufacturers or logistics companies that rely on certain conditions to operate.

-

Cyber Insurance

In today’s digital world, this is more critical than ever. Unfortunately, fraud and attacks occur daily despite a business’s best efforts. This covers data breaches, hacking, cybercrime, and system recovery. Many companies neglect to put this cover in place and forget about their privacy obligations to their customers. A hacking event could result in legal action quickly bankrupting a business.

-

Commercial Property Insurance

Protects your buildings, equipment, and contents from events like fire, theft, or damage. This is an obvious one, but many businesses have insufficient coverage and risk major losses.

-

Product Liability Insurance

If you manufacture or sell products, this covers damage or injury caused by faulty products. Depending on the product type and nature of your industry, this can be highly costly, and you must discuss with your broker which insurer is best.

-

Management Liability / Directors & Officers Insurance

This insurance covers legal costs and claims against business owners or directors in case of mismanagement, breach of duty, or regulatory investigations. Mainly targeted at larger businesses, as your organisation grows, you need to consider the challenges of overseeing all facets and protecting yourself from legal issues and loss.

👉 Need Help and Advice With Your Business Insurance? Get Help Here.

Choosing the Right Insurance Broker

Like in all professions, brokers vary in quality and knowledge depending on the types of businesses they work with.

A good insurance broker has access to a broad range of products and has strong relationships with insurers to fight for your claim when needed or negotiate custom terms.

✅ Industry Experience – Choose a broker who understands the risks specific to your industry.

✅ Licensing & Independent– Ensure they’re properly licensed (check via ASIC’s professional register) and not tied to a single insurer. This is essential to ensure you get a broad range of options.

✅ Claims & Ongoing Support/Review – A good broker is a partner in your business. They don’t just put a policy in place. They will ask questions about your plans for the year and advise you when they need to be involved, e.g., if you plan to buy five new pieces of equipment or are expanding your staffing. They need to ensure you are covered for your current plans. Before renewal, they shouldn’t simply send you an invoice, they will ask you what has changed, research your updated industry risks, ask you your plans for the year ahead and make a new assessment.

✅ Clear Communication – Your broker should explain your cover in plain English and help you understand what is claimable and where you may have gaps to mitigate in other ways.

✅ Customised Solutions – Beware of ‘one size fits all’ packages. Your business is unique and has its own risks. There is no point in paying for insurance if you cannot claim it when needed!

👉 Need Help and Advice With Your Business Insurance? Get Help Here.

Why Do Premiums Go Up? (And How to Keep Them Down)

Insurance premiums are continually climbing, with many providers becoming more risk-averse or restrictive, particularly for higher-risk industries.

The good news is that premiums are often driven by factors you can influence, including having a documented risk management plan and controls you can prove to an insurer.

Here’s what causes increases:

🚫 Claims history – Multiple or high-value claims can flag your business as a high risk. We have seen several instances where premiums have nearly doubled due to an unfortunate year for a business owner that was out of their control.

Whilst equipment/property claims are more common, a business with multiple work health and safety-related issues leading to workers’ compensation claims (including for mental health) may struggle to get a policy. Not being able to obtain insurance will either mean accepting a very expensive option or having doors closed!

🚫 Incorrectly valuing assets – Not accurately valuing property or stock can lead to higher future premiums or ot having sufficient cover in the event of a claim.

🚫 Poor risk management – Brokers and insurers will ask you about your Work Health & Safety plans. If you don’t have one or don’t have supporting technology to enforce these policies and protect against security threats, your premiums and ability to successfully claim can be impacted.

🚫 Market conditions—Economic pressures, natural disasters, risks specific to your industry, and global insurance trends can also impact your business.

Don’t worry, though, you can take steps to become a lower risk and score lower premiums:

✅ Implement safety protocols, documen,t and automate them

✅ Where you have had a history of claims, document and create a detailed plan to ensure it does not happen in the future, and success stories with specific examples showing how your plan helped you avoid other potential claims. Have this ready for your next renewal to negotiate.

✅ Maintain property and equipment properly & have detailed records for the ongoing maintenance

✅ If you’re confident you won’t have regular claims, you can increase your excess to reduce premiums

✅ Invest in cybersecurity and data protection. Have a document with details of your cyber management plan ready to produce for insurers.

✅ Demonstrate business stability and growth. Growing businesses with minimal claims are ideal for insurers. Make sure you review your options with multiple insurers to avoid paying ‘loyalty tax’.

The more professional and proactive you appear to insurers, the more negotiating power you and your broker have.

MANDATORY Annual Reviews

Too often, SME’s set and forget their insurance or accept renewal notices without question, only to find out that they’re underinsured, overpaying, or exposed to a significant risk.

An annual insurance review with your broker is critical for:

📌 Capturing business changes – Have you grown, expanded services or product lines, hired new staff, or moved premises? Your policy needs to reflect that.

📌 Avoiding coverage gaps – Laws, risk, and your industry evolve. Your cover should too.

📌 Identifying cost savings – You might be paying for outdated or unnecessary cover or missing bundled savings (where you have multiple insurance policies with a single insurer).

📌 Planning for growth – As your business scales, your insurance strategy should support and protect that growth.

Think of it as a financial checkup. It’s about protecting your success, not just covering your risks.

Final Word: Good Insurance is Good Business

Insurance isn’t a grudge purchase. It’s an investment in your business’s resilience and long-term success. With the right broker and a proactive approach, you’ll be better protected, more confident, and financially stronger.

Need a trusted insurance broker who understands your business inside out? Contact us, and we’ll connect you with industry-aligned professionals who can help you get covered and get ahead.