Running a small business in Australia often means confronting a persistent reality: growth costs money before it makes money. Whether you’re buying equipment, expanding premises, hiring staff, or bridging a cash-flow gap, accessing capital at the right time can mean the difference between seizing an opportunity and watching it pass.

Secured small business loans are one of the most powerful financing tools available to Australian business owners. By pledging an asset as collateral, you can typically access larger sums at lower interest rates than unsecured alternatives — making them especially attractive for established businesses with assets on hand.

This guide explains everything you need to know: how secured loans work, what lenders look for, which lenders are worth considering, and how to put together an application that stands the best chance of success.

👉 Checkout the best secured small business finance options here.

What Is a Secured Small Business Loan?

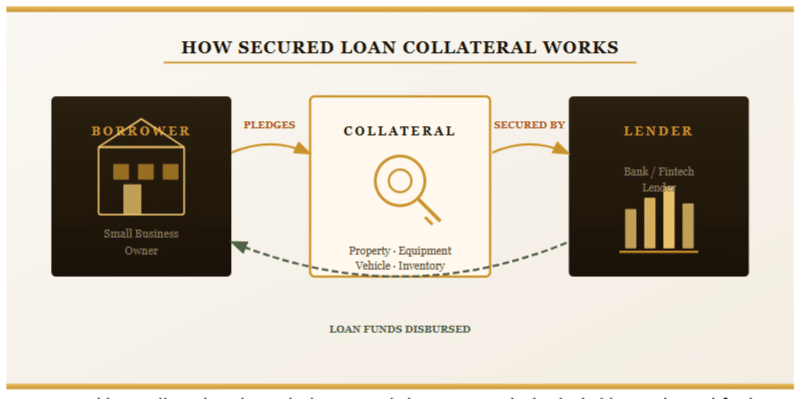

A secured small business loan is a form of business finance where the borrower pledges one or more assets — known as collateral or security — to the lender. If the borrower defaults on repayments, the lender has the legal right to seize and sell the pledged asset to recover the outstanding debt.

Because the lender has a tangible backstop, they are generally willing to offer:

- Higher borrowing limits (often $500,000 to $5 million+)

- Lower interest rates compared to unsecured products

- Longer repayment terms, sometimes up to 25 years for property-secured loans

- More flexible qualifying criteria, especially for businesses with limited credit history

In Australia, secured business loans are offered by the major banks (Commonwealth, ANZ, NAB, Westpac), non-bank lenders, and a growing ecosystem of fintech platforms — each with different products, rates, and approval criteria.

How Secured Business Loans Work in Australia

The mechanics of a secured business loan in Australia follow a straightforward process. You apply with a lender, nominate an asset as security, and if approved, receive a lump sum (or line of credit) which you repay over an agreed term with interest.

Lenders will register their security interest over your nominated asset on the Personal Property Securities Register (PPSR), or in the case of real estate, via a mortgage registered with the relevant state or territory land titles office. This legal registration means the lender’s claim on the asset is publicly recorded and takes priority in the event of insolvency.

Repayments are typically structured as monthly instalments covering both principal and interest. Some products offer interest-only periods — common in property-secured loans — followed by principal-and-interest repayments.

Important: Most secured business loans require a personal guarantee from the business director(s) in addition to the asset security. This means your personal assets may also be at risk if the business defaults. Always seek independent legal advice before signing.

Types of Collateral Accepted by Australian Lenders

The asset you pledge as security is central to any secured loan application. Australian lenders typically accept the following categories of collateral:

Residential or Commercial Property

Real estate is the most commonly accepted — and most highly valued — form of collateral. Lenders will typically lend up to 70–80% of the property’s value (the Loan-to-Value Ratio, or LVR). Both residential and commercial properties are accepted, though residential real estate often attracts better terms due to its higher liquidity.

Business Equipment and Machinery

Specialist lenders offer secured loans against business equipment — excavators, trucks, medical devices, commercial kitchen equipment, and more. These are commonly structured as chattel mortgages or equipment finance, where the lender retains a security interest in the equipment itself.

Vehicles

Commercial vehicles, fleets, and heavy vehicles are widely accepted as collateral. Loan terms typically match the useful life of the vehicle — usually three to seven years.

Business Assets and Inventory

Some lenders will accept a General Security Agreement (GSA) over the totality of a business’s assets — including stock, receivables, and equipment. This is more common with non-bank and specialist lenders.

Term Deposits and Investment Portfolios

Cash-backed security using term deposits or share portfolios is accepted by some lenders, often enabling very competitive interest rates due to the low risk profile of liquid assets.

Pros and Cons of Secured Business Loans

| Factor | Secured Loan | Unsecured Loan |

| Interest Rate | Lower (6–15% p.a.) | Higher (15–40%+ p.a.) |

| Loan Amount | Up to $5M+ | Usually capped at $500K |

| Loan Term | Up to 25 years | Usually 1–5 years |

| Asset Risk | Asset at risk if default | No direct asset risk |

| Application Speed | Slower (valuation required) | Faster (days not weeks) |

| Eligibility | More accessible with assets | Stronger credit required |

Eligibility Requirements

While requirements vary by lender, most Australian banks and non-bank lenders will assess the following when evaluating a secured business loan application:

- Time in business: Most lenders require at least 12–24 months of trading history.

- Annual turnover: Typically a minimum of $75,000–$150,000 per year, though this varies widely.

- Credit score: Both your business and personal credit scores will be assessed. Most lenders prefer a score above 550, though property-secured loans have more flexibility.

- Collateral value: The asset must be independently valued and meet the lender’s minimum LVR requirements.

- Financials: Up to two years of business tax returns, BAS statements, and profit and loss statements are typically required.

- Business structure: Sole traders, partnerships, companies (Pty Ltd), and trusts are all generally eligible, though documentation requirements differ.

Interest Rates and Fees to Expect

Secured business loan interest rates in Australia typically range from 6% to 15% per annum, depending on the type of collateral, loan-to-value ratio, and your overall credit profile. Property-secured loans tend to sit at the lower end of this range, while equipment and vehicle loans typically attract slightly higher rates.

Beyond the interest rate, watch for the following fees when comparing products:

- Establishment/application fee: $0–$2,000+, sometimes charged as a percentage of the loan

- Valuation fee: $300–$1,500+ depending on the asset type and location

- Ongoing monthly fee: $10–$50 per month with some lenders

- Early repayment fee: Can be significant with fixed-rate loans — check the break cost formula

- PPSR registration fee: A small government fee for registering the security interest

- Legal/mortgage fees: For property-secured loans, solicitor fees for mortgage documentation

Always calculate the comparison rate, not just the headline rate. The comparison rate includes most fees and gives a truer picture of the loan’s total cost.

Top Lenders Offering Secured Business Loans in Australia

The Australian business lending market spans the major banks, regional banks, non-bank lenders, and fintech platforms. Here’s an overview of the main options:

- Commonwealth Bank (CBA): Australia’s largest bank offers secured business loans from $10,000 to $5M+. Strong for property-secured lending with competitive rates for established businesses.

- NAB Business Banking: Well-regarded for SME lending, with dedicated business bankers and strong equipment finance capabilities. Suitable for businesses with $500K+ turnover.

- ANZ Business Loans: Offers secured term loans and overdrafts backed by property or business assets. Good for agribusiness and commercial property sectors.

- Westpac Business Finance: Offers secured loans, equipment finance, and commercial property loans. Strong branch network suits businesses who prefer face-to-face service.

- Pepper Money: A leading non-bank lender with more flexible credit criteria, suitable for business owners with imperfect credit history.

- Moula, Prospa, OnDeck: Fintech lenders offering fast-turnaround loans ideal for smaller amounts ($10K–$500K) where speed matters.

A business finance broker can help you access the full market — including lenders not available directly — and may negotiate better terms on your behalf.

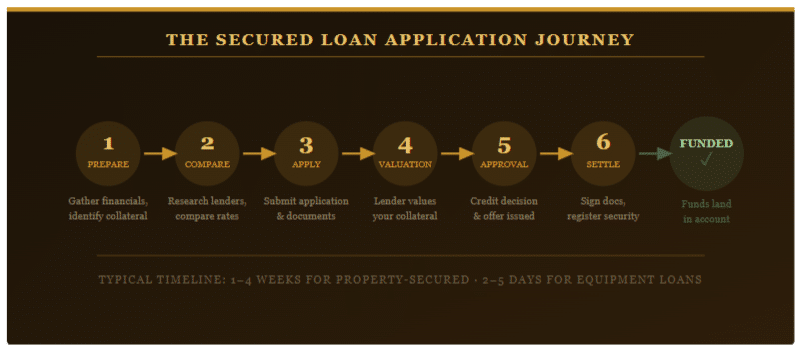

How to Apply: Step-by-Step

Step 1: Clarify Your Borrowing Purpose

Lenders want to know exactly why you need the funds. Having a clear and documented purpose — ideally with supporting quotes or contracts — strengthens your application significantly.

Step 2: Assess Your Collateral

Identify which assets you’re prepared to offer as security and get a preliminary sense of their value. For property, recent comparable sales or a desktop valuation can give you an early estimate.

Step 3: Prepare Your Financial Documents

Gather the last two years of business and personal tax returns, BAS statements, profit and loss statements, a balance sheet, and recent bank statements (typically three to six months).

Step 4: Check Your Credit File

Request a free copy of your business and personal credit reports from agencies like Equifax, illion, or Experian before applying. Identify and address any errors or overdue accounts.

Step 5: Compare Lenders or Engage a Broker

Use comparison sites and speak to a commercial finance broker to understand what’s available. Different lenders specialise in different collateral types.

Step 6: Submit Your Application

Submit your application with all required documentation. Incomplete applications create delays. Be prepared for the lender to request additional information around the valuation of your collateral.

Step 7: Review the Offer and Negotiate

If you receive an offer, don’t accept immediately. Review the comparison rate, fees, early repayment clauses, and any restrictive covenants. Rates and fees are often negotiable for well-qualified borrowers.

Alternatives to Secured Business Loans

A secured loan isn’t always the right fit. Depending on your circumstances, the following alternatives may be worth considering:

- Unsecured business loans: Faster approval, no collateral required, but higher rates and lower limits. Suitable for short-term cash flow needs under $200,000.

- Business line of credit: A revolving facility ideal for managing working capital rather than funding a one-off purchase.

- Invoice finance: Borrow against your unpaid invoices. No property required; your debtors are effectively the security.

- Equipment finance / chattel mortgage: Purpose-built for asset purchases — the equipment itself is the security, keeping your property free.

- Government grants and loans: The Australian federal and state governments offer a range of grants and loans for small businesses. Check business.gov.au for current programs.

Frequently Asked Questions

Can I get a secured business loan with bad credit?

Yes — this is one of the main advantages of secured lending. If you have strong collateral (particularly property with significant equity), some lenders will approve applications despite poor credit history. Non-bank lenders like Pepper Money are more likely to consider these applications than the major banks.

How long does it take to get approved?

Equipment and vehicle loans from fintech lenders can be approved in as little as 24–72 hours. Property-secured loans typically take two to four weeks due to the valuation process and legal mortgage documentation.

What happens if I can’t repay the loan?

If you miss repayments, the lender will typically issue a formal default notice and allow a period (often 30 days) to remedy the breach. If the default continues, the lender can enforce their security — meaning they can seize and sell the collateral.

Is the interest on a secured business loan tax deductible?

Generally yes — interest paid on loans used for business purposes is deductible under Australian tax law. Speak with your accountant about the specific treatment for your situation.

Do I need a business plan to apply?

For smaller loans (under $250,000), a formal business plan is rarely required. For larger amounts with the major banks, a business plan and cash flow projections can meaningfully strengthen your application.