Not every business owner has property to pledge or assets to put on the line. And not every funding need can wait three weeks for a valuation and mortgage paperwork. For Australian small business owners who need capital quickly — or who simply don’t want to risk their assets — unsecured business loans have become one of the most accessible and widely used financing options in the market.

Unsecured small business loans require no collateral. You borrow based on the strength of your business’s cash flow, revenue, and creditworthiness alone. The trade-off is higher interest rates and lower borrowing limits compared to secured lending — but for the right use case, that trade-off is entirely worthwhile.

This guide covers everything you need to know: how unsecured loans work, who qualifies, what you’ll pay, which lenders are worth considering, and how to give your application the best possible chance of approval.

👉 Checkout the best unsecured small business finance options here.

What Is an Unsecured Small Business Loan?

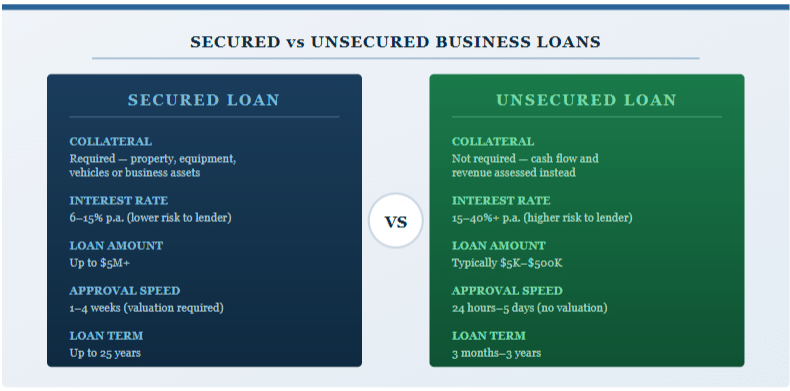

An unsecured small business loan is a form of business finance where the lender provides funds without requiring the borrower to pledge any specific asset as security. There is no mortgage, no chattel, no registered charge over equipment or property — the lender relies on the business’s financial performance and credit profile to assess the risk of lending.

Because the lender has no asset to fall back on if the borrower defaults, unsecured loans carry a higher risk from the lender’s perspective. This is reflected in:

- Higher interest rates than equivalent secured products

- Lower maximum loan amounts (typically capped at $500,000, often less)

- Shorter repayment terms (usually 3 months to 3 years)

- More stringent trading history and revenue requirements

Despite these trade-offs, unsecured loans remain enormously popular with Australian small businesses precisely because of what they don’t require: no property to risk, no lengthy valuation process, and in many cases, approval within 24–48 hours.

It’s worth noting that most unsecured business loans still require a personal guarantee from the business director(s). This means that while no specific asset is pledged upfront, you remain personally liable for the debt if the business cannot repay. This is an important distinction — unsecured does not mean consequence-free.

How Unsecured Business Loans Work in Australia

The application and funding process for an unsecured business loan is considerably simpler and faster than for secured lending. Here’s how it typically works:

You apply with a lender — either directly or through a broker — providing information about your business revenue, trading history, and cash flow. The lender assesses your application using a combination of your financial data, business credit profile, and personal credit score. Many fintech lenders also connect directly to your accounting software (Xero, MYOB) or bank account data via open banking to make this assessment in real time.

If approved, funds are typically deposited within 24–48 hours. Repayments are usually structured as daily, weekly, or monthly instalments over the loan term, with interest calculated either as a flat factor rate or an annual percentage rate (APR) depending on the lender.

Unlike a secured loan, there is no PPSR registration, no mortgage documentation, and no valuation process — which is precisely why the turnaround is so fast.

Who Is an Unsecured Loan Best Suited For?

Unsecured business loans are not a one-size-fits-all solution, but they are particularly well-suited to:

- Businesses without significant assets — service businesses, consultancies, digital agencies, and professional practices that operate with few tangible assets

- Businesses needing fast capital — opportunities that require a quick decision, such as a bulk stock purchase, a short-term contract requiring upfront outlay, or an urgent equipment repair

- Business owners who don’t want to risk property — particularly those who have a family home they are unwilling to put up as collateral

- Short-term cash flow gaps — managing the lag between invoicing and payment, covering payroll during a slow period, or bridging a tax liability

- Established businesses with strong revenue — lenders weight revenue and cash flow heavily for unsecured loans, so businesses with consistent turnover above $100,000–$150,000 per year are well-positioned

Conversely, unsecured loans are generally less suitable for funding long-term capital investments, property purchases, or large equipment acquisitions — where the lower interest rates and longer terms of secured finance make considerably more sense.

Eligibility Requirements

Because unsecured lenders have no collateral to fall back on, they assess your application more heavily on the financial health of your business. Common eligibility criteria across Australian unsecured lenders include:

- Time in business: Most lenders require a minimum of 6–12 months of trading history. Some fintech lenders will consider businesses from 3 months, though terms will be less favourable.

- Minimum monthly revenue: Typically $5,000–$10,000 per month, though this varies by lender and loan size. Some lenders set an annual turnover minimum of $75,000–$100,000.

- Credit score: Both personal and business credit scores are assessed. Most mainstream unsecured lenders prefer a personal credit score above 500–550. Some specialist lenders will consider lower scores at higher rates.

- Australian business registration: The business must be registered in Australia (ABN required). Most lenders also require the business to be registered for GST if turnover exceeds the threshold.

- Personal guarantee: Almost universally required. The director(s) of the business must personally guarantee the loan.

- No active bankruptcies: Current or undischarged bankruptcy of a director typically disqualifies an application with most lenders.

Interest Rates, Fees, and True Cost of Borrowing

Understanding the true cost of an unsecured business loan requires looking beyond the headline interest rate. Unsecured business lending in Australia uses several different pricing structures, which can make comparisons tricky.

Annual Percentage Rate (APR)

The most transparent pricing structure. The interest rate is expressed as an annualised percentage of the outstanding balance. A $100,000 loan at 20% APR over 12 months costs roughly $20,000 in interest (though this varies with the amortisation schedule).

Factor Rate

Commonly used by fintech and short-term lenders. A factor rate is a multiplier applied to the principal — for example, a factor rate of 1.25 on a $50,000 loan means you repay $62,500 in total, regardless of how quickly you repay. Factor rates do not reduce with early repayment, making them more expensive if you repay ahead of schedule.

Fees to Watch For

| Fee Type | Typical Range | Notes |

|---|---|---|

| Establishment / origination fee | 1.5–3% of loan amount | Often deducted from funds upfront |

| Monthly account fee | $0–$50/month | Varies widely by lender |

| Early repayment fee | Nil–remaining interest | Factor rate loans often charge remaining interest regardless |

| Late payment fee | $25–$100 per event | Plus potential default interest |

| Broker / referral fee | 1–4% of loan amount | Paid by lender, not borrower, in most cases |

The most reliable way to compare unsecured business loans is to calculate the total repayment amount — the sum of all repayments over the life of the loan — rather than relying on the advertised rate alone.

Types of Unsecured Business Finance in Australia

The term “unsecured business loan” covers a broad range of products. Understanding the differences helps you choose the right structure for your needs.

Term Loan

A lump sum disbursed upfront and repaid in fixed instalments over an agreed term. Best for one-off investments or purchases where you know the exact amount required. Terms typically range from 3 months to 3 years for unsecured products.

Business Line of Credit

A revolving credit facility where you draw down funds as needed up to an approved limit, and only pay interest on what you use. Highly flexible and well-suited to managing ongoing cash flow rather than funding a specific purchase. Limits typically range from $10,000 to $250,000 for unsecured facilities.

Merchant Cash Advance

A lump sum advance repaid as a percentage of your daily card sales or revenue. Repayments flex with your income — slower when sales are slow, faster when they’re strong. Popular with hospitality, retail, and other businesses with high card transaction volumes. Generally the most expensive form of unsecured finance.

Invoice Finance (Unsecured Variant)

Some invoice finance products operate without a formal security agreement over the debtor book. You advance against outstanding invoices and repay when the client pays. Fast and flexible, but limited to businesses with B2B invoice-based revenue.

Business Credit Card / Overdraft

Bank-issued credit facilities that technically qualify as unsecured business lending. Useful for small, recurring expenses and short-term float but expensive for anything requiring sustained borrowing due to high revolving interest rates.

Top Unsecured Business Loan Lenders in Australia

The unsecured business lending market in Australia is dominated by fintech lenders, though the major banks also offer unsecured facilities — typically to existing customers with strong banking relationships.

- Prospa: One of Australia’s most established fintech lenders. Offers unsecured loans from $5,000 to $150,000 with terms up to 36 months. Known for fast approvals and a straightforward online application process. Suitable for businesses with 6+ months trading history.

- Moula: Focuses on data-driven lending using accounting software and open banking. Loans from $5,000 to $250,000. Strong on transparency and competitive on rates for well-qualified applicants.

- OnDeck Australia: Offers term loans and lines of credit up to $250,000. Uses proprietary scoring to assess applications quickly. Good for businesses that may not qualify with traditional banks.

- Lumi: Australian-founded lender offering unsecured loans up to $500,000 for established businesses. One of the higher limits available in the unsecured space.

- Capify: Specialises in merchant cash advances and short-term unsecured loans. Good option for hospitality and retail businesses with strong card turnover.

- Commonwealth Bank (CommBiz Unsecured): The major banks offer unsecured overdrafts and business loans, typically to existing customers. Rates are more competitive but approval criteria are stricter and turnaround slower.

- NAB QuickBiz: NAB’s fast unsecured loan product for existing customers, offering up to $100,000 with same-day decisions for eligible businesses.

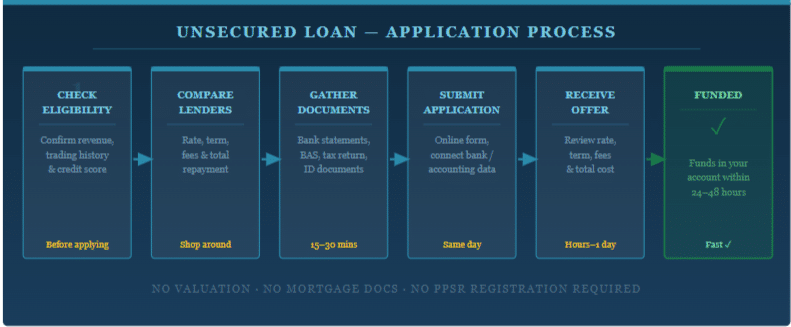

How to Apply for an Unsecured Business Loan

The unsecured business loan application process — from eligibility check to funded, typically within 24–48 hours.

Step 1: Check Your Eligibility Before Applying

Review the lender’s minimum requirements for trading history, monthly revenue, and credit score before submitting a formal application. Every hard credit enquiry leaves a mark on your credit file — multiple applications in a short period can negatively impact your score and reduce your chances of approval.

Step 2: Calculate How Much You Actually Need

Borrow only what you need. Because unsecured interest rates are higher than secured alternatives, unnecessary borrowing is expensive. Be specific about the purpose and amount, and stress-test the repayments against your current cash flow before committing.

Step 3: Prepare Your Documents

Most unsecured lenders require: 3–6 months of business bank statements, your most recent business tax return or BAS statements, proof of ABN registration, and director ID. Many fintech lenders also accept a direct connection to Xero, MYOB, or your bank via open banking — which can speed up assessment significantly.

Step 4: Compare Total Repayment, Not Just Rate

Given the variety of pricing structures used by unsecured lenders, always ask each lender for the total repayment amount and the effective APR. This allows apples-to-apples comparison regardless of whether the lender uses a factor rate, monthly rate, or annual rate.

Step 5: Read the Personal Guarantee Terms Carefully

Before signing, understand exactly what you are personally guaranteeing. Some guarantees are limited (capped at the loan amount); others are unlimited and may extend to legal costs and default interest. If in doubt, have a solicitor review the guarantee before you sign.

Tips to Improve Your Approval Chances

- Maintain clean bank statements: Lenders scrutinise 3–6 months of transaction data. Avoid overdrafts, dishonoured payments, and erratic cash flow in the period before you apply.

- Reduce existing debt obligations: A high ratio of existing debt repayments to revenue (debt service coverage) is a red flag for unsecured lenders. Pay down what you can before applying.

- Check and address your credit file: Request a free credit report from Equifax, illion, or Experian and fix any errors before applying.

- Use a broker: A good business finance broker has access to a panel of lenders and can match your profile to the most appropriate product — improving your approval odds and potentially saving you significant money in interest.

- Apply for the right amount: Applying for more than your revenue can comfortably service is a common reason for rejection. Most lenders cap repayments at 15–25% of monthly revenue.

👉 Checkout the best unsecured small business finance options here.

Alternatives to Unsecured Business Loans

If an unsecured loan doesn’t quite fit your situation, the following alternatives are worth exploring:

- Secured business loan: If you have property or equipment available as collateral, a secured loan will almost always deliver a lower interest rate, higher borrowing limit, and longer term.

- Invoice finance: If your cash flow gap is caused by slow-paying clients, invoice finance lets you advance up to 80–85% of the invoice value immediately — without taking on a traditional loan.

- Equipment finance / chattel mortgage: If the purpose is to purchase equipment or a vehicle, equipment finance uses the asset itself as security, usually at far better rates than an unsecured loan.

- Business overdraft: For recurring, short-term cash flow needs, a bank overdraft attached to your business transaction account may be cheaper than a term loan — you only pay interest when you use it.

- Government-backed loans: Programs such as the federal government’s SME Guarantee Scheme (when active) and various state-based business loan programs offer subsidised or guaranteed lending. Check business.gov.au for current availability.

Frequently Asked Questions

Can I get an unsecured business loan as a sole trader?

Yes — sole traders are eligible for unsecured business loans in Australia. You will need a valid ABN, typically at least 6–12 months of trading history, and will be assessed on your personal and business financials combined. As a sole trader, your personal credit score carries significant weight in the assessment.

What is the maximum I can borrow with an unsecured business loan?

Most Australian unsecured lenders cap loans at $250,000–$500,000, with the majority of approvals for small businesses falling in the $20,000–$150,000 range. The amount you qualify for depends on your monthly revenue — most lenders will approve up to 1–1.5 times your monthly turnover.

Does applying for an unsecured loan affect my credit score?

Yes — most lenders conduct a hard credit enquiry as part of the application process, which temporarily reduces your score by a small amount. Multiple applications in a short period compound this effect. Use a broker to identify the most suitable lender before applying, rather than submitting multiple applications simultaneously.

How is an unsecured business loan different from a personal loan used for business?

An unsecured business loan is assessed against your business’s financial performance and is structured for business use. A personal loan is assessed against your personal income and credit profile. Business loans generally offer higher limits and terms more suited to commercial purposes. Using a personal loan for business also creates complications for tax deductibility and accounting.

Are unsecured business loan interest rates tax deductible?

Yes — interest paid on a business loan used for business purposes is generally tax deductible in Australia, regardless of whether the loan is secured or unsecured. Speak with your accountant about the correct treatment for your business structure.

What happens if my business can’t repay an unsecured loan?

If the business defaults, the lender will pursue recovery through the personal guarantee. This means the director(s) become personally liable for the outstanding balance. The lender may obtain a court judgment, which can then be enforced against personal assets including bank accounts, vehicles, and property. Defaulting on a business loan also damages both your business and personal credit files, affecting your ability to borrow in future.