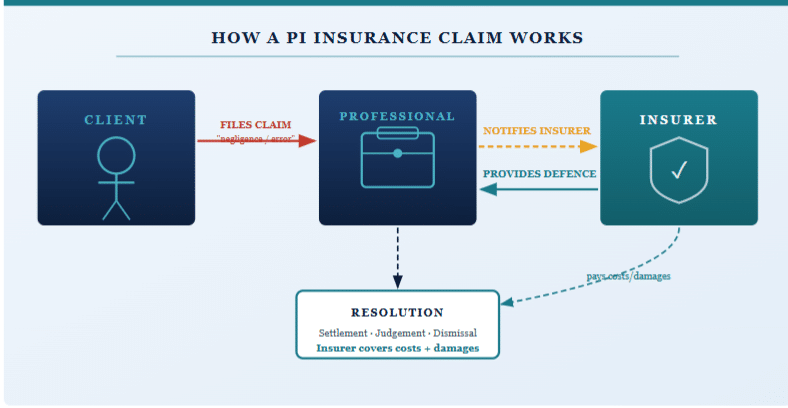

A single client complaint. An alleged oversight in advice. A contract dispute over deliverables. For Australian professionals, any of these scenarios can trigger a legal claim that costs tens — or even hundreds — of thousands of dollars to defend, regardless of whether the allegation is valid.

Professional Indemnity (PI) insurance exists precisely for this reason. It protects professionals from the financial consequences of claims alleging negligence, errors, omissions, or breach of professional duty in the services they provide. In many industries it is now legally mandatory. In virtually all others, it is commercially essential.

This guide walks through everything you need to know about PI insurance in Australia — from the fundamentals of what it covers, to how policies are structured, what you’ll pay, and how to choose the right level of protection for your profession.

👉 Need Help and Advice With Your Business Insurance? Get Help Here.

What Is Professional Indemnity Insurance?

Professional Indemnity insurance is a form of liability insurance that protects professionals and businesses against claims made by clients who allege that the professional’s advice, service, or work caused them financial loss, harm, or damage.

Unlike public liability insurance — which covers physical injury or property damage — PI insurance is specifically concerned with the financial and reputational harm that can flow from professional advice or services. A financial planner whose investment recommendation causes a client to lose money, an architect whose design contains a structural flaw, or an IT consultant whose implementation causes a data breach — all could face PI claims.

A quality PI policy typically covers:

- Legal defence costs (often the largest component of any claim)

- Compensation awarded to the claimant

- Investigation and expert witness costs

- Court and tribunal fees

- Settlements negotiated on your behalf by the insurer

Crucially, most PI policies cover the cost of defending a claim even if the allegation ultimately proves unfounded. In litigation-heavy professional sectors, this protection alone can justify the premium.

Who Needs PI Insurance in Australia?

Any individual or business that provides professional advice, consultancy, or specialist services to clients should seriously consider PI insurance. The core question is simple: could a client suffer financial loss as a result of your advice or work? If the answer is yes, you have PI exposure.

Professions that commonly require or benefit from PI insurance include:

- Legal professionals — solicitors, barristers, conveyancers (mandatory via state law societies)

- Financial advisers — AFSL holders (mandatory under ASIC licensing requirements)

- Architects and engineers — mandatory in most states; high-value claims common in construction

- Healthcare professionals — doctors, dentists, allied health (registration often requires PI cover)

- Real estate agents — mandatory via state licensing; errors in disclosure or valuations common

- IT and technology consultants — system failures, data breaches, and project overruns generate claims

- Accountants and auditors — CPA Australia and CA ANZ both require members to hold PI cover

- Management consultants — strategy, HR, and operational consultants face growing claim frequency

- Surveyors and valuers — property valuation errors can carry enormous downstream financial impact

Increasingly, clients and government contracts require proof of PI coverage before engaging a professional. If you tender for government work in Australia, PI insurance is almost universally mandatory at the pre-qualification stage.

What Does PI Insurance Cover?

Negligence Claims

The most common basis for PI claims. If a client alleges that your advice or service fell below the reasonable standard expected of a competent professional and caused them financial loss, the policy responds. This includes errors made in good faith as well as unintentional omissions.

Breach of Professional Duty

Claims alleging that you failed to meet a specific professional obligation — whether arising from legislation, professional codes of conduct, or contractual undertakings — are covered under most PI policies.

Defamation (in a Professional Context)

Some PI policies extend to cover defamation claims arising from statements made in the course of professional services — for example, an adverse reference or a report containing inaccurate statements about a third party.

Intellectual Property Infringement

Accidental breach of copyright, trademark, or other intellectual property rights in the course of delivering professional services is covered under many modern PI policies.

Loss of Documents

The accidental loss, destruction, or damage of client documents — physical or digital — and the costs associated with their reconstruction is a standard PI extension.

Legal Defence Costs

Legal fees to defend even a meritless claim can run to $50,000–$200,000. Most PI policies cover these costs in addition to (not deducted from) the limit of indemnity, though some policies are “defence costs inclusive” — an important distinction to check.

What Is Not Covered?

Understanding exclusions is just as important as understanding what’s covered. Common PI policy exclusions in Australia include:

- Intentional misconduct or fraud: Deliberate wrongdoing is universally excluded.

- Criminal fines and penalties: Regulatory fines, criminal sanctions, and punitive damages are generally not covered.

- Employment disputes: Claims from your own employees fall under Management Liability or Employers Liability cover, not PI.

- Pre-existing circumstances: Claims arising from circumstances you were aware of before the policy incepted and failed to disclose are excluded.

- Bodily injury and property damage: Physical injury to persons or damage to tangible property falls under Public Liability insurance.

- Business activities outside the policy scope: Services not described in your policy schedule may not be covered.

Critical disclosure warning: Australian PI policies are underwritten on the basis of utmost good faith. You are legally required to disclose all material facts — including any known circumstances that could give rise to a claim — when applying or renewing. Failure to disclose can void your policy entirely.

When Is PI Insurance Mandatory in Australia?

| Profession / Category | Requirement Source | Typical Minimum Cover |

|---|---|---|

| Financial Advisers (AFS Licensees) | Corporations Act 2001 / ASIC | $2 million per claim |

| Solicitors & Barristers | State law society rules | $1.5M–$10M depending on state |

| Registered Architects | Architects Acts (state-based) | $1 million (varies by state) |

| Registered Tax Agents | Tax Agent Services Act 2009 | $250,000 per claim |

| Real Estate Agents | State property licensing laws | $500,000–$1M (varies by state) |

| Migration Agents | Migration Agents Regulations | $250,000 per claim |

| Health Practitioners | AHPRA registration standards | Varies by profession/scope |

PI insurance is legally required for a significant and growing number of professions in Australia. Requirements are imposed by federal legislation, state licensing laws, or professional association rules.

How Much Does PI Insurance Cost in Australia?

PI insurance premiums vary considerably based on profession, revenue, claims history, and chosen coverage limits. The table below provides indicative premium ranges for common professions.

| Profession | Annual Revenue | Cover Limit | Indicative Annual Premium |

|---|---|---|---|

| IT Consultant (sole trader) | $150,000 | $1M | $600–$1,200 |

| Management Consultant (small firm) | $500,000 | $2M | $1,800–$3,500 |

| Accountant (sole trader) | $200,000 | $1M | $900–$1,800 |

| Financial Adviser | $300,000 | $2M | $3,000–$8,000 |

| Architect | $400,000 | $5M | $4,000–$9,000 |

| Solicitor (boutique firm) | $600,000 | $5M | $5,000–$14,000 |

Key factors that influence your premium include your profession’s claims history as a sector, your individual claims history, annual revenue, number of employees, and whether you handle client money or assets.

How Claims-Made Policies Work — and Why It Matters

Almost all Australian PI policies are written on a “claims-made” basis. This means the policy that responds to a claim is the one active at the time the claim is made, not the one in force when the underlying work was carried out.

This has two critical practical implications:

Retroactive Date

Your PI policy will include a retroactive date — the earliest point in time from which your past work is covered. Claims arising from work performed before this date are excluded. When you first take out PI insurance, your retroactive date should be set as far back as possible — ideally to when you first began practising. Never allow this date to move forward when switching insurers.

Run-Off Cover

When you retire, close your business, or change careers, your PI policy ends — but your exposure to past work does not. A client can bring a claim years after the work was completed. Run-off cover maintains protection for claims that arise after your policy ends, for work done while it was active. This is essential when ceasing practice.

How to Choose the Right PI Policy

Limit of Indemnity

Set your limit with reference to the maximum plausible loss a client could sustain from your work — not just the size of your typical engagement. Large professional firms often carry $10M–$20M in limits; sole traders typically carry $1M–$2M.

Defence Costs: Inside or Outside the Limit?

Some PI policies pay legal defence costs in addition to the limit of indemnity (outside the limit). Others count defence costs against the limit (inside the limit). Outside-the-limit policies provide substantially better protection and are worth seeking out.

Policy Excess

The excess is the amount you contribute to each claim before the insurer pays. Excesses typically range from $500 to $25,000+. Ensure your excess is affordable given your working capital — paying it upfront can be a strain during an already stressful claims event.

Scope of Covered Activities

Check that all of your professional activities are explicitly described in the policy schedule. If you have expanded your services since last renewal, notify your insurer and ensure the new activity is covered.

Insurer Financial Strength

An insurer with an “A” or higher credit rating from a recognised agency (AM Best, S&P, Moody’s) provides greater confidence that claims will be paid. APRA-regulated insurers must maintain minimum capital adequacy standards.

Leading PI Insurers in Australia

- QBE Insurance: One of Australia’s largest PI insurers with strong coverage for professional services, construction professionals, and healthcare.

- Chubb: A global specialist insurer with deep PI expertise. Particularly strong for financial services professionals, lawyers, and technology firms.

- Berkley Insurance Australia: A specialist professional lines insurer with competitive offerings for SME professionals including consultants, accountants, and IT specialists.

- CGU (IAG): Major domestic insurer offering PI through brokers and professional associations. Popular with sole traders and small practices.

- Dual Australia: A managing general agent specialising in professional and management liability with strong digital platforms and competitive rates.

- AIG Australia: Strong in financial institutions PI, D&O combined products, and technology sector coverage.

- BizCover / Gallagher / Aon: Insurance intermediaries that allow professionals to compare and purchase policies from multiple underwriters — useful for sole traders seeking competitive rates.

👉 Need Help and Advice With Your Business Insurance? Get Help Here.

Frequently Asked Questions

Is PI insurance tax deductible in Australia?

Yes. PI insurance premiums paid for the purpose of producing assessable income are generally tax deductible under Australian tax law. Consult your accountant to confirm the treatment for your structure.

What’s the difference between PI and Public Liability insurance?

Public Liability covers claims for physical injury to third parties or damage to their property. PI covers financial loss arising from professional advice or service failure. Most professionals operating a physical workspace need both.

What happens if I have a claim after switching insurers?

Because PI policies are claims-made, what matters is which policy is active when the claim is made. If you switch insurers, ensure your new policy’s retroactive date covers the period of the prior work. Never allow a retroactive date to move forward.

Can I get PI insurance if I’ve had a prior claim?

Yes, although prior claims will affect your premium and may affect the terms offered. Full disclosure of any prior claims is mandatory at renewal or new application. A specialist broker can be particularly valuable in this situation.

How much PI cover do I actually need?

A useful starting point is the maximum loss any single client could suffer as a result of your work. Also consider contractual minimums specified by clients, regulatory minimums for your profession, and the likely cost of defending a claim — legal fees alone can exhaust a low limit of indemnity.

Do I need PI insurance as a contractor?

If you provide professional services under contract, you likely have PI exposure. Many contractors incorrectly assume they’re covered under their client’s policy. In most cases, they are not. Review your contracts carefully and obtain your own PI cover.